How can we get more dollars to diverse asset managers & founders?

We can rethink school endowment management.

Diverse companies are a good investment: on average, they have higher revenues per dollar raised, better financial returns, and faster exits than homogeneous teams.

They also consistently receive less than 5% of all venture capital funding all together.

Investment firms tend to support like entrepreneurs. For example, firms with at least one female partner are 2x more likely to fund female founders and 3x more likely to fund companies with female CEOs than firms with all male partners are. But as of 2019, white men still managed about 99% of the $7 trillion U.S. asset management industry (which includes hedge funds, private equity, and venture capital). At this rate, it will take about 200 years for female asset managers to achieve equal status.

How can female, BIPOC, Latinx, and other diverse asset managers and, subsequently, diverse founders access these investment dollars?

One solution is to rethink school endowment management.

Background:

“Endowments” refer to schools’ financial assets, which they invest to increase the amount of money at their disposal. To find the best opportunities — those that make the most money off their original investment — schools may have an internal investment office and/or give part of their endowment to financial firms, trusting those external asset managers to invest it successfully.

In July 2020, Congressmen Emanuel Clever II (D-MO) and Joseph Kennedy III (D-MA) wrote to the 25 U.S colleges and universities with the biggest endowments. Concerned that women and minorities weren’t represented proportionally in asset management and inspired by the systematic discrimination, exclusion, and inequality shown through the killing of George Floyd, the Congressmen asked each school how it was trying to improve diversity within its internal investment teams and any external U.S-based asset managers it had hired.

By gathering this information, the Congressmen aimed to ensure that endowments, which the federal government subsidizes, were spent in accordance with “public interest” and in compliance with the “numerous laws prohibiting discrimination in university operations”. But, to the Congressmen, investing with diverse managers was both a moral and fiduciary duty:

The unfounded proposition that investing with diverse-owned firms occurs at the expense of returns is both insulting and contrary to academic research and empirical findings. In fact, expanding the pool of talent under consideration and seeking differentiated investment strategies is a hallmark of prudent investing. Universities that miss opportunities to allocate to high-performing diverse managers due to bias in sourcing or firm assessment may be violating fiduciary obligations by failing to generate those returns for their endowment.

In short, increasing diversity and inclusion are necessary and advantageous: they help institutional investors, like colleges and universities, start mitigating a historical lack of representation and expanding opportunities for often overlooked but high-performing diverse managers.

Studies have shown that diverse-owned investment firms — those with women and/or minorities owning 25% or more of the firm — have returns equal to or greater than those of firms that aren’t diverse-owned. Venture capital specific research found that VCs that increased their proportion of female partner hires by 10% saw, on average, a 1.5% improvement in annual fund returns and a nearly 10% increase in profitable exits.

And yet, diverse-owned firms manage about a penny for every dollar managed by firms owned by white men.

Select Results:

Future Recommendations:

In the fall of 2020, the Congressmen published the “Cleaver/Kennedy Report”, which included the data they collected, recommendations for the future, and concrete steps for schools to improve their diversity and inclusion practices.

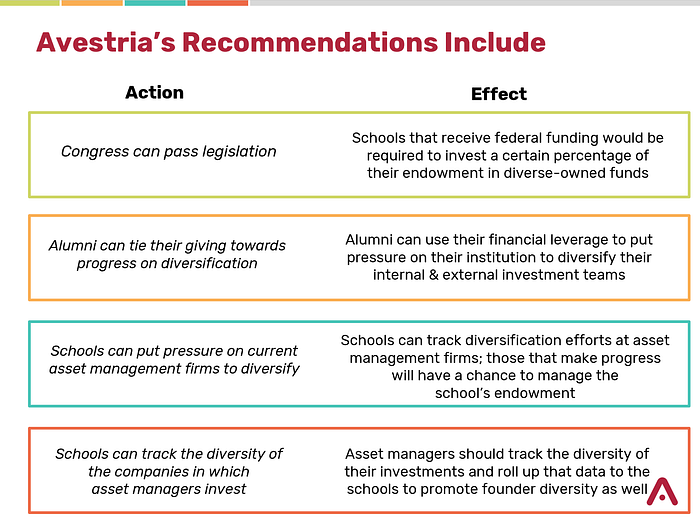

The team at Avestria Ventures — a female-owned and -led venture capital firm — have several recommendations of our own to add to the Congressmen’s:

→ Congress can pass legislation requiring schools that receive federal funding to invest a certain percentage of their endowment in diverse-owned firms.

→ Alumni can tie their giving towards their alma mater’s progress on making and meeting diversity requirements. While the average alumni giving rate for the 2018–2019 academic year was 8%, that number can be higher, especially for Ivy League alumni — and Ivy League schools have some of the biggest endowments. Princeton, for example, reported an average two-year alumni giving rate of 55%: a number that demonstrates alumni’s significant financial leverage.

→ Schools can put pressure on current asset management firms to diversify their ranks. In October 2020, on behalf of Yale’s Investment Office, David F. Swensen (1954–2021) sent a survey on hiring, training, mentoring, and retaining diverse talent to U.S-based firms managing Yale’s endowment. Firms that don’t show annual progress could lose the opportunity to manage part of Yale’s $31.2B endowment.

→Schools should track allocations both to those managing the endowment investments and those receiving the investments. As the Congressmen recommended, schools should look at the individuals holding leadership positions and making decisions within asset management teams — but asset managers should do the same with potential investments. These two data sets should be shared with the investing school to ensure that both those managing the allocations and those receiving the allocations reflect diversity and represent the most financial potential.

Conclusion:

As the Congressmen wrote,

Although diverse managers have historically faced extreme levels of overt bias and discrimination — continuing to impact the allocation of capital today — institutional investors have an opportunity to correct the legacy of systemic exclusion and expand opportunities for high performing diverse asset managers. Colleges and universities who consider investments with these underutilized and often overlooked diverse managers stand to improve returns on investment and drive social impact.

We believe that the Congressmen’s approach would have a waterfall effect: rethinking school endowment management can allow not only for an increased number of women and other diverse asset managers to manage endowment funds but also for women and other diverse founders to access these funds.

Going forward, we hope that schools’ diversity data continues to be tracked, published, and publicized and that this progress will allow everyone — including the school, its internal investment committee, its external asset managers, and the founders of the companies in which it invests — to benefit.